- Our Bond sales team adds six new customer relationships in the last three months and expands two existing accounts.

- Long-term potential with the six new customer relationships could reach $16 million in annual recurring revenue. Further expansion with two existing customers could add another $4 million.

- OBAI could be undervalued against the Company’s success in market penetration and footprint expansion.

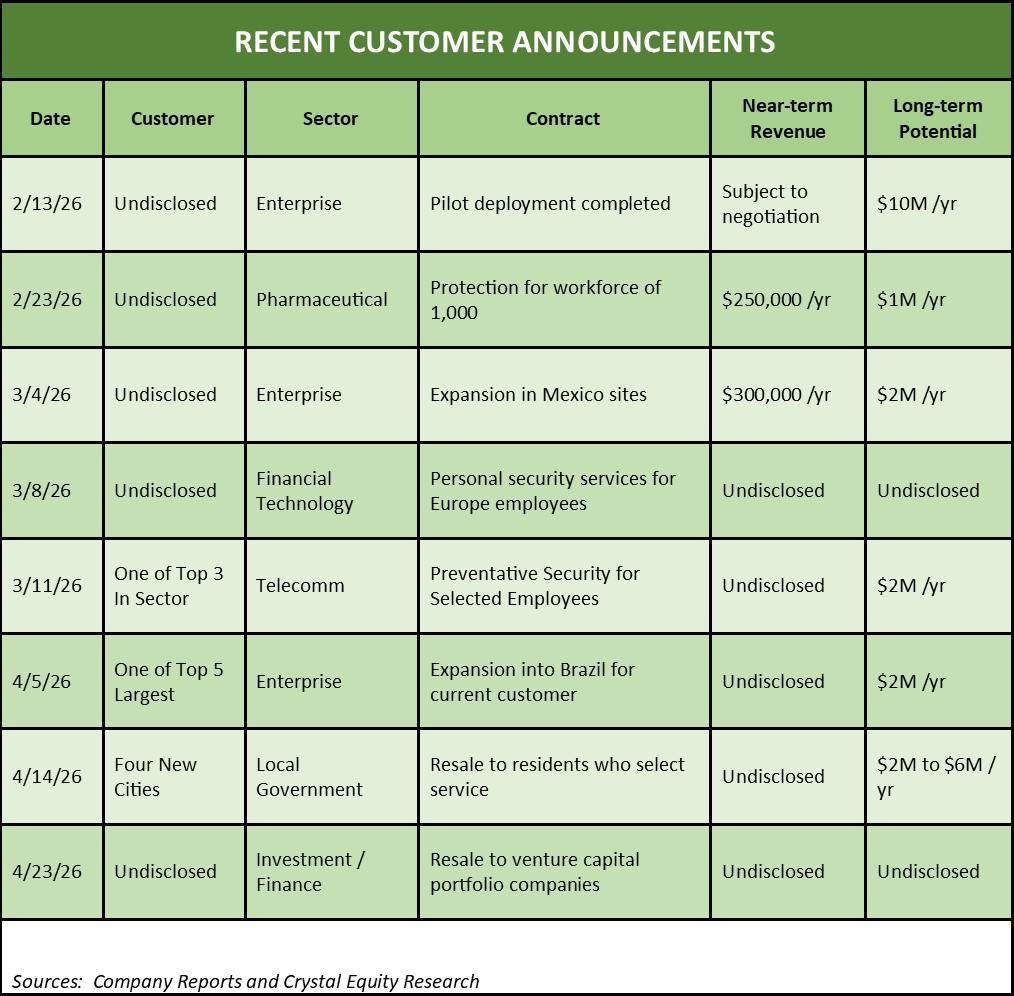

Since our introduction of Our Bond, Inc., with the February 2026 post “AI Driven Personal Security Solution”, the sales team has planted one flag after another in the fast-growing market for preventative security services. As shown in the table below, over the last three months the group has landed six new customers and expanded two accounts. The Company is a bit circumspect about its customers. No company names are disclosed and, in some cases, even near-term sales value is kept under wraps. Indeed, Our Bond might be ill advised to signal competitors with too many details on interest in modern personal security services.

Consequently, some investors might not have fully appreciated the importance of these new and expanded customer relationships to OBAI valuation. For Our Bond, recurring revenue is the key to achieving profitability and building earnings as the cost of customer retention is significantly lower than new customer acquisition. Potential recurring revenue streams from these eight customers alone could reach as much as $20 million per year.

Of course, it will take time to realize the full potential from each account. So far, the Our Bond team has done well, with nearly 100% customer retention. That success should give investors greater confidence in the Company’s ability to grow its revenue line by expanding customer relationships. Indeed, two of the eight announcements listed in the table below involve existing customers that are extending service coverage.

It is also noteworthy that Our Bond entered a new geography, Brazil, and established a foothold in an additional sector, financial services. Both accounts are likely to attract new eyes to Our Bond’s profile, augmenting other business development investments.

Both new customers are members of highly lucrative market opportunities. Industry research firm, Market Research Future, cited in a recent report on the Brazil security services market, a surge in demand for technology integrated security solutions. The days are probably gone when adequate physical security for employees can be assured by a lone guard near reception.

Likewise, fintech companies, like Our Bond’s new customer in Europe, are at the forefront of a rise in ever larger campus-style business centers. Larger corporate campuses encompass data centers, energy infrastructure, employee amenities and transportation hubs, all of which need protection. The European Central Bank reports that the fintech sector in the European Union has doubled in last decade, clustering in large financial centers.

Currently, OBAI trades at 0.72 times trailing revenue. At that multiple, an additional $20 million at the top line is thus worth as much as $14 million in incremental market value, more than double the current market capitalization of $10.7 million. Before anyone gets carried away with the big numbers, it must be remembered that customer account expansion could take years, not weeks or months. Nonetheless, investors can view OBAI as undervalued at the current price relative to the Company successful market penetration and footprint expansion.

Neither the author of the Small Cap Strategist web log, Crystal Equity Research nor its affiliates have a beneficial interest in the companies mentioned herein.

Underwriters of the Prime series may have a beneficial interest in, serve as agents of, or act as advisors to the companies mentioned herein.