- Cloudastructure among first movers using artificial intelligence (AI) technology in an innovative site security application

- Proprietary site security solution delivering impressive results in terms of effective threat identification and intervention

- Strong initial market penetration within multifamily residential sector as eight of the top fifteen property management companies have adopted the Cloudastructure solution

- Large market opportunities in multiple verticals such as multifamily residential property, truck/trailer parking services and other commercial properties

- Shelf registration statement recently filed with the SEC provides quick access to the capital market when management decides to accelerate market penetration or invest in new product technology

- Undervalued stock after dramatic market reaction to shelf registration and market worries about negative impacts of AI technology

Cloudastructure, Inc. (CSAI: Nasdaq) provides remote site security solution featuring cloud-based video surveillance and centralized monitoring agents. Real-time video analysis is aided by artificial intelligence (AI) and machine learning technologies. The remote agents can deal with the issue directly, notify property managers and/or alert local police and fire responders.

During the year 2025, over 98% of threatening activity identified by the platform was ultimately deterred. A good share of this successful outcome is due to the efficiency and effectiveness of the AI-based platform to simultaneously monitor in real time all video from all cameras. The result is more rapid and more thorough identification of threat activity. Real-time human intervention is more rapidly triggered. Cloudastructure’s innovation central to cloud-based computer vision for video surveillance and analytics is protected by a U.S. patent.

Initial Market – Multi-family Residential Property

Management has targeted the multi-family residential sector, one of the most prominent property types in the U.S. There are approximately 44 million multi-family housing units in the U.S., representing as much as 30% of the housing stock in the U.S. Urbanization and increased interest in rental over ownership is driving demand for apartments, condominiums and townhouses. Indeed, the multi-family alternative is growing at 9.4% annually, nearly three times the rate of single-family homes at 3.2% annually. (Statistica, ThisOldHouse.com, Cushman and Wakefield).

Apartment complexes are busy places, with residents coming and going at all hours of the day and night. It is not surprising then that perceived crime rates at U.S. multi-family housing units have increased in recent years compared to the country as a whole. In 2024, the Federal Bureau of Investigation reported 359 violent crimes and 1,760 property crimes for every 100,000 people in the U.S., representing a 5.4% decrease from the previous year. By contrast, a survey of multi-family property managers completed in early 2025, found that 25% of respondents reported 25% increase in property and violent crime.

The increasing crime trend is a call to action for property managers. Crime threatens occupancy rates, the driving force behind profits. Tenants worry about safety, so much so that even competitively priced properties are passed over. Property owners are also plagued by increasing expenses for tenant compensation, property repairs and insurance coverage.

The use case for a remote site security service like that of Cloudastructure is aided by comparison to the high costs of undetected crime. Furthermore, the Company’s sales team can cite their system’s successful threat recognition rates compared to conventional on-site guards and human video monitoring.

So far eight of the top fifteen multi-family property management companies have said yes to the Cloudastructure solution. The top five of the Company’s customer list represents 1.2 million residential units, just the tip of the market ‘iceberg.’ Widening of these relationships is a significant growth opportunity for the Company. Indeed, in early February 2026, Cloudastructure announced an expansion of its partnership with a multi-family housing owner in the Southeastern U.S. from one property to four properties.

Expansion to New Verticals

Truck parking operators are another type of commercial property where remote security solutions are in strong demand. The American Transportation Research Institute estimates there are as many as 310,000 truck parking sites in the U.S., of which about half are private facilities. These parking sites serve an estimated three million truckers nationwide, who are looking for safe locations to store valuable tractors and trailers while resting or awaiting a return trip.

In late 2025, the Company scored its first service agreement with a commercial truck parking operator. Management indicates the customer considered several alternatives. Cloud storage of video footage and the ability to scale nationally helped differentiate the Cloudastructure solution.

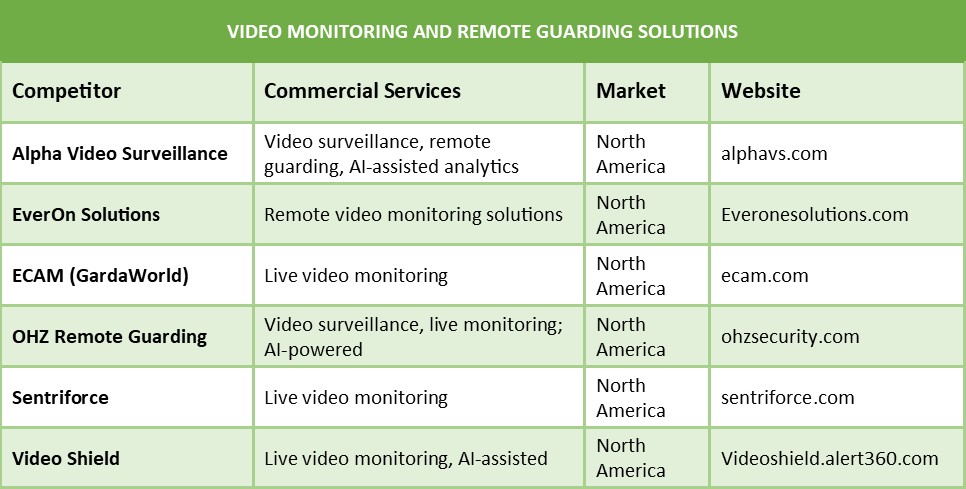

Competition, Comrades

The market for site security solutions is highly fragmented, differing in scope and solution types. The range of contenders varies from on-site guard units to in-house camera and monitor systems to other remote video monitoring services. Furthermore, not all security providers operate nationwide. Thus, direct competitors can vary from region to region and from sector to sector.

A building track record of excellent results and a cost-effective fee structure have helped the Cloudastructure solution stand out in the crowd. Success rates in threat detection and resolution may be particularly helpful if customers are making comparisons to rivals that also offer remote video monitoring. We note that the appearance of other similar rivals could be helpful in situations where an old technology – on-site guards and video monitoring – is poised to be replaced by a new technology – video surveillance driven by AI analytics in the cloud. Prospects may see the presence of multiple rivals as an endorsement of the trend.

Sales Ramp, Profit Leverage

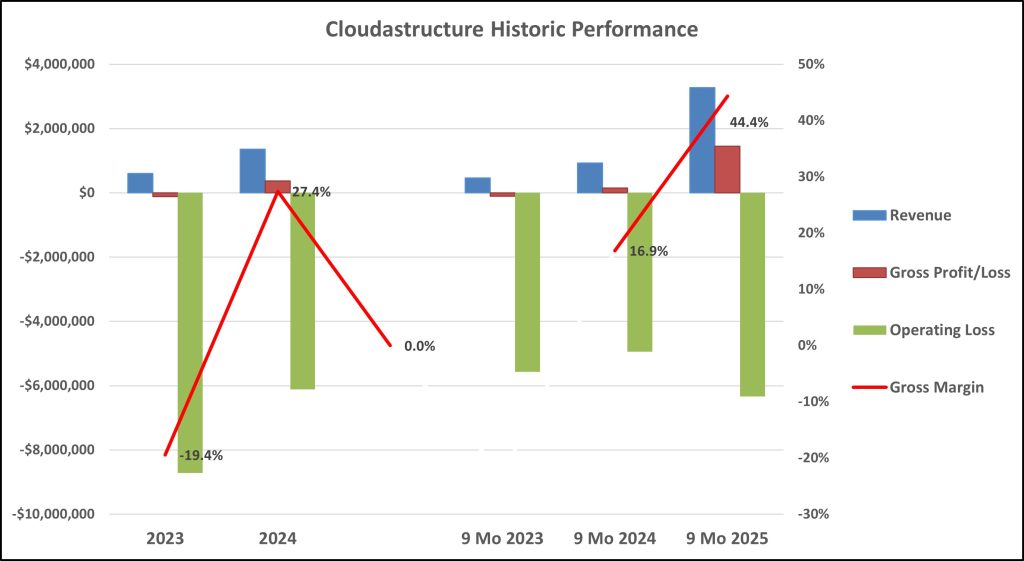

Cloudastructure’s success in entering its initial target market of multi-family housing properties, can be seen in its most recent financial results as reported in filings with the SEC. In the nine months ending September 2025, the Company clocked in $3.3 million in total sales, three and a half times the sales activity in the same period of the previous year. Better utilization of the Company’s cloud installation can be observed in gross profit margin improvement to 44.4% in the partial year 2025, compared to 16.9% in the same period of the prior year. A chart of historic financial results reveals a picture of rising sales and gross profits.

Operating expenses increased in the first nine months of 2025, to $7.8 million, representing a 52.7% increase year-over-year. Nonetheless, against the higher revenue level, the operating expenses as a percentage of sales decline to 238% of total sales in the first nine months of 2025. This represented significant improvement over 526% in the same period the year before.

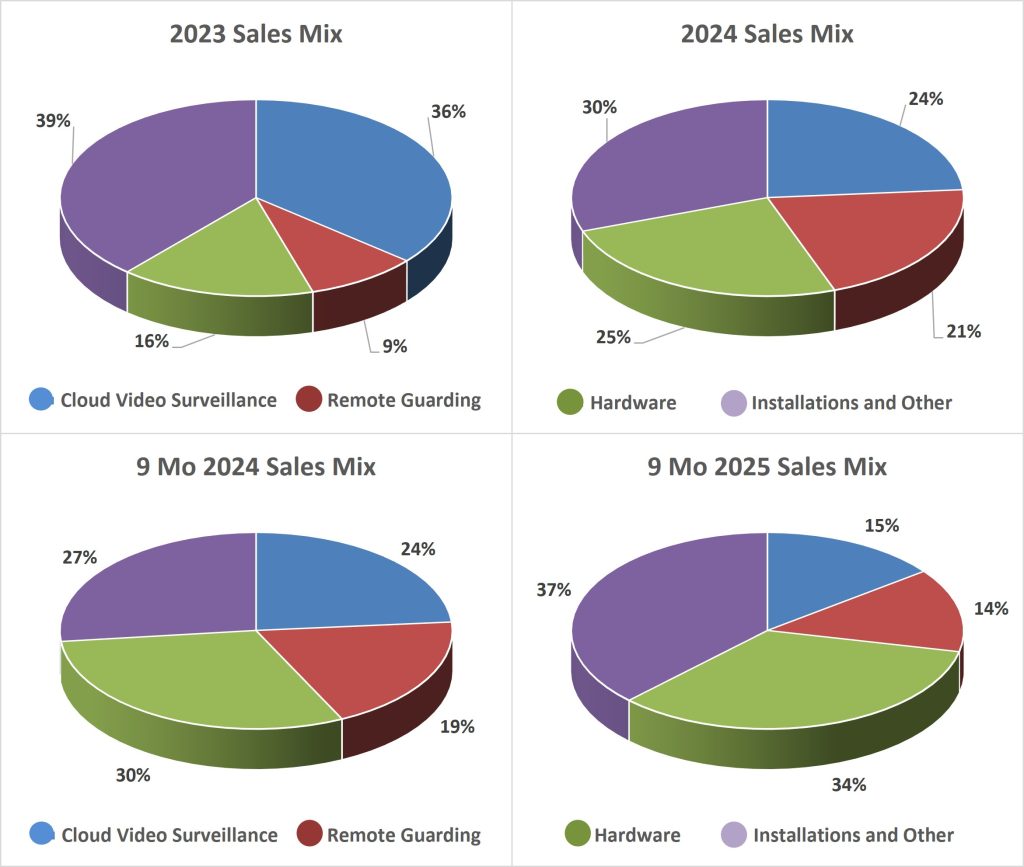

Revenue is broken down in four categories: Hardware, Installations, Cloud Video Surveillance and Remote Guarding. The Company accepts most hardware installed at a customer’s site, as long as the system produces video of sufficient resolution, there are still hardware needs related to video upload and transfer. Hardware and Installation revenue increased as a portion of the mix in the full year 2024 compared to the prior year, continuing to ramp in the first nine months of 2025. Installations are, of course, a precursor to future recurring sales from Cloud Video Surveillance and Remote Guarding.

Indeed, Cloud Video Surveillance and Remote Guarding are bright spots in Cloudastructure’s growth and profit potential. Surveillance grew by 47.6% in 2024 over the prior year and accelerating in the first nine months of 2025 to 120.7% year-over-year growth. The sales ramp delivered strong profit leverage. The gross profit margin on Surveillance sales increased to 54% in the first nine months of 2025, as the expanded activity level increased utilization of the Company’s data center. Likewise Remote Guarding realized increasing efficiency, with a gross profit margin of 63% in the first nine months of 2025, compared to 57% in the year-ago period.

What to Expect

Management indicates a goal to report financial results for the full year 2025, in early March 2026. Investors will have a chance to confirm favorable trends in top-line growth and steady profit margin improvement. Expansion at the top line appears to be accelerating as year-over-year growth in sales was 372% in the quarter ending September 2025, the fastest rate in the Company’s history. The gross profit margin in the quarter was 49.7%, the widest quarter profit since inception.

Based on the recent pace of sales activity and direct costs, revenue could reach $5.0 million for the full year 2025, providing as much as $1.2 million in gross profit. Unfortunately, given the requirements of the Company’s marketing and sales program and the need to continue research and development, investors will have to wait for profits. The operating loss for the full year could reach $8.0 million.

The Company may need a sales run rate near $6.0 million per quarter to reach breakeven in the period. This assumes management keeps a tight grip on spending, which is not easy given the attractiveness of the remote guarding market to new competitors. Good news, the recent pace of revenue growth could deliver the required sales level by the end of 2026.

Dose of Reality

Even with operational breakeven the Company may not reach positive cash flow. In the nine months ending September 2026, Cloudastructure used $5.7 million in cash resources to support operations. Of course, operating expenses were the primary use of cash, but the situation was made worse by some billings getting bogged down in accounts receivable.

Thus, adequacy of cash resources is a paramount concern. At the end of September 2025, the Company reported a cash kitty of $6.4 million. Based on recent cash usage rates, the bank account probably gave the Company about a one-year runway before the bus sputters to a stop.

To gas up, management has alternatives. There are already two established new capital resources: a $40 million equity line of credit and more recently an at-the-market sales agreement to place $50 million in common stock. Cost is a factor in tapping either resource, providing incentive to explore alternatives. Accordingly, in late December 2025, the Company filed a shelf registration statement with the SEC for $150 million in various equity securities or debt.

Dilution Worries, Depressed Share Price

Unfortunately, it appears investors kicked up some dust over the prospect of dilution represented by the shelf registration. In early February 2026, when the registration statement was declared effective by the SEC, CSAI shares were sold off. Ironically, the reduced share price makes a capital raise less attractive and therefore less likely.

The price movement has reduced price multiples to 4.1 times sales and 2.8 times book value. This is the most attractive valuation in over a year. CSAI could be an attractive play on applied AI for contrarian investors with a tolerance for risk and the patience to wait for the business model to play out. In the near term, dilution will be a factor as the Company takes on new capital to support market penetration. Large market opportunities, top-line growth, and the appearance of profit leverage suggests the chance to deliver positive cash flow and earnings – allowing the Cloudastructure to ‘grow into’ its outstanding stock.

Neither the author of the Small Cap Strategist web log, Crystal Equity Research nor its affiliates have a beneficial interest in the companies mentioned herein.

Underwriters of the Prime series may have a beneficial interest in, serve as agents of, or act as advisors to the companies mentioned herein.